Agentic Commerce in 2026

Protocols, trust, payments, and how money will move in an agentic world

A working view of how AI agents are starting to buy things for people, how the underlying stack is evolving, and where the biggest opportunities are emerging.

Contents

2. Why now?

4. The stack

6. Protocols

16. Closing thoughts

For the last twenty years, online shopping has worked in roughly the same way. You search for a product, open a few tabs, compare options, and eventually type your card details into a checkout form. Almost every part of the commerce stack assumes there is a human sitting in front of a screen.

Agentic commerce changes who does the shopping.

Imagine telling an AI agent:

“Keep our office stocked with coffee. Spend less than £500 per month. Use approved suppliers.”

Instead of just recommending products, the agent finds suppliers, compares prices, places orders, and handles repeat purchases. You set the goal and the rules. The agent does the work.

That sounds like a small change. It isn’t.

As soon as software starts spending money on behalf of people and businesses, almost every layer of commerce has to adapt. Product catalogs need to be structured so machines can understand them. Payment systems need ways to authorise and monitor autonomous purchases. Fraud systems need to distinguish trusted agents from malicious bots. Merchants need to decide which agents can access inventory, place orders, and complete transactions.

This is why agentic commerce is much bigger than “AI shopping assistants”. It is forcing a redesign of the infrastructure underneath online commerce.

To understand what is happening, it helps to look at three questions.

First, how do agents talk to merchants, marketplaces, and payment networks?

Second, how does everyone trust a non-human piece of software to move money?

Third, where is value being created as commerce becomes increasingly agent-driven?

The rest of the article walks from the basics to the stack, then to what is live today, what is still missing, and how money will move in an agentic world.

1. What agentic commerce is (and what it isn’t)

At its simplest, agentic commerce means software that can buy things on your behalf.

That sounds obvious, but it is a meaningful shift from the assistants and chatbots people are used to today.

Take the office coffee example from the introduction. The interesting part is not that the agent can recommend a supplier. It is that the agent can decide what to buy, place the order, and spend money within a set of rules.

Three things make this different from traditional ecommerce.

First, the agent has some freedom. It is choosing between real options rather than following a fixed script.

Second, the agent can execute. It does not stop at recommendations. It can add items to carts, select shipping options, and trigger payments.

Third, the rest of the system recognises who the agent represents. Merchants, payment providers, and banks need to know whether they are interacting with Alice’s shopping agent, a procurement agent acting for a business, or an unknown bot.

This distinction matters. A smarter search box or a chatbot that recommends products but still requires you to complete the purchase is not really agentic commerce. The interesting problems only begin once software can actually spend money.

2. Why now

The idea of software buying things for people is not new. Subscription refills, recurring purchases, and “buy it again” buttons have existed for years.

What changed is that the technology finally became capable enough to handle more open-ended tasks.

Modern AI models can browse websites, use tools, reason across multiple steps, and maintain context throughout a workflow [1]. Instead of following a predefined path, they can navigate real-world purchasing decisions.

At the same time, the infrastructure around them has started to mature.

New commerce protocols such as the Universal Commerce Protocol (UCP) and Agentic Commerce Protocol (ACP) give agents a standard way to interact with merchants. New authorisation standards such as AP2 define how users can delegate purchasing authority to agents. Card networks are building trust layers such as Visa’s Trusted Agent Protocol (TAP) to distinguish approved agents from malicious automation.

User behaviour is changing as well.

More product discovery is starting inside ChatGPT, Gemini, Perplexity, and AI-powered search experiences rather than traditional search engines. Adobe reported a 1,300% year-over-year increase in holiday ecommerce traffic coming from generative AI platforms, highlighting how quickly these interfaces are becoming part of the shopping journey [2].

For the first time, the pieces are starting to line up. The models are capable enough, the standards are emerging, and users are increasingly comfortable interacting with AI systems throughout the buying process.

3. Why the first wave fell short

A few years ago, the pitch was simple.

Agents would find deals, manage subscriptions, and buy things while you slept.

The reality has been messier.

There are plenty of impressive demos, but relatively few examples where an agent can reliably go from intent to payment without handing control back to a human.

The interesting thing is that the bottleneck is no longer the models.

Modern AI systems are already capable of understanding requests, comparing options, and navigating workflows. The harder problems sit elsewhere.

The reasons are mostly boring.

Product data is messy. Catalogues are incomplete, inconsistent, and often missing the information agents need to make decisions.

Most ecommerce systems were built for browsers, not autonomous software. APIs are inconsistent, websites change frequently, and workflows contain countless edge cases designed around human behaviour.

Fraud systems are another challenge. For years, “bot” and “fraud” were almost interchangeable concepts inside many risk teams. Agentic commerce requires merchants and payment providers to distinguish between malicious automation and authorised software acting on behalf of a real customer.

Permissions are equally unclear. If an agent is allowed to buy coffee for the office, how much can it spend? Which suppliers can it use? How often can it place orders? Until recently there were no standard answers to those questions.

The result is an infrastructure problem rather than a model problem.

Identity, permissions, trust, payments, checkout, and data standards all need to work before agents can transact reliably at scale.

Much of the work happening across the industry today is no longer about making models smarter. It is about building the plumbing that allows those models to act safely and reliably in the real world.

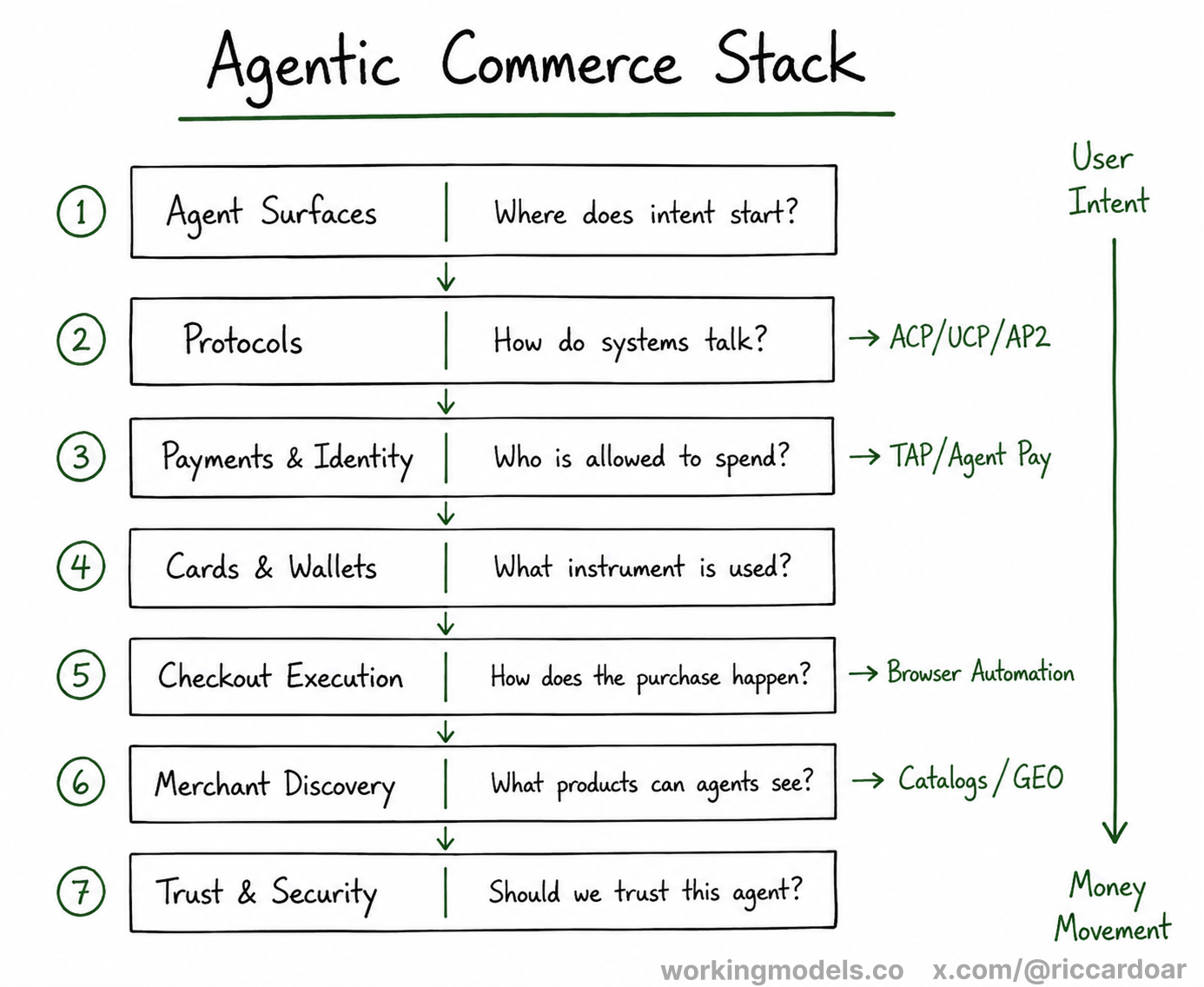

4. A simple mental model of the stack

At this point it helps to stop thinking about “agentic commerce” as a single thing.

Let’s go back to our coffee example.

You tell an agent:

“Keep our office stocked with coffee. Spend less than £500 per month. Use approved suppliers.”

That sounds like a simple request. In reality, it touches almost every part of the commerce stack.

The agent needs a place to receive instructions. It needs a way to discover products and suppliers. It needs permission to spend money. It needs a payment instrument. It needs a way to complete checkout. Merchants need a way to recognise and trust it. And everyone involved needs a record of what happened if something goes wrong.

This is why it helps to think about agentic commerce as a stack of layers.

Every serious agentic commerce flow touches most of these layers.

The protocol debates mostly sit in the second layer. Payments and identity live in the middle of the stack. Trust and fraud cut across almost everything. Many of the most interesting startups are building between layers rather than inside a single one.

The rest of this article walks through the stack from top to bottom.

5. Layer 1 – Where journeys start: agent surfaces

The top of the stack is where people interact with agents.

In the traditional web, that meant opening Google, browsing websites, and comparing products yourself.

In an agentic world, the starting point increasingly becomes a conversation.

Instead of searching for products directly, users describe what they want:

“Find me a four-star hotel near King’s Cross for under £150.”

or

“Buy a coffee machine for a twenty-person office.”

The agent then translates that intent into actions further down the stack.

This layer matters because whoever owns the interface often owns the customer relationship. These systems decide which merchants are visible, which product feeds are available, and which protocols are supported underneath.

There are two broad categories of agent surfaces emerging today.

The first is general-purpose AI interfaces such as ChatGPT, Gemini, Perplexity, and AI-powered search experiences. These systems handle a growing share of product discovery and can work across many categories.

The second is vertical agents that focus on a single workflow. Travel is one of the most advanced examples, with companies such as Layla, MindTrip, and Wanderboat building agents that can help users plan and book trips. Fashion has a similar wave of companies including Daydream, Doji, Alta, and Look.ai.

The difference is depth. General agents try to help with many tasks. Vertical agents go much deeper into a specific workflow and often integrate directly with booking systems, inventory systems, or business software.

Most of these products still hand users off to traditional checkout flows, but they are increasingly becoming the place where buying decisions start.

6. Layer 2 – Protocols: ACP, UCP, AP2, TAP

Agent surfaces are where journeys begin.

But eventually an agent needs to do more than understand intent. It needs to search catalogues, build carts, place orders, and trigger payments.

Today, most websites expose this information through pages designed for humans. Agents can scrape those pages, but that approach is fragile and difficult to scale.

This is the problem commerce protocols are trying to solve.

Instead of forcing agents to interpret websites, protocols give merchants, marketplaces, payment providers, and agents a shared language.

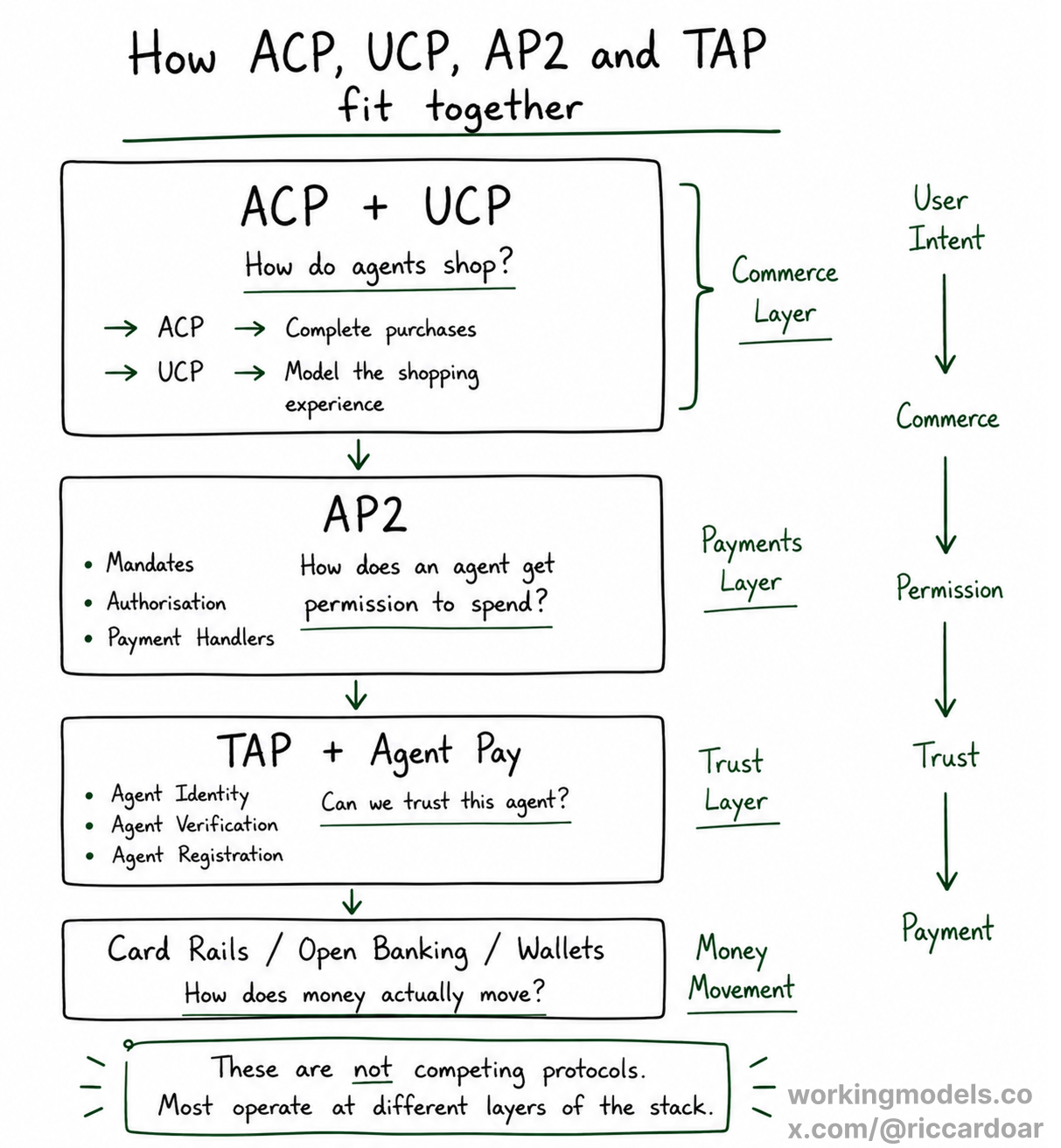

One way to think about these protocols is that they do for agentic commerce what HTTP did for the web: they give different systems a standard way to communicate.

Today, four protocols are attracting most of the attention.

6.1 ACP – Agentic Commerce Protocol

ACP is an open standard co-developed by Stripe and OpenAI, with Meta also listed as a creator in Stripe’s docs [3].

Its goal is simple: give agents a standard way to complete purchases.

It defines a standard way for agents to browse product feeds, build carts, delegate payments, and receive order updates.

ACP already powers “Instant Checkout” experiments in ChatGPT: agents can fill a cart, and Stripe issues Shared Payment Tokens so ChatGPT can trigger payments on a user’s behalf without exposing card numbers [4].

6.2 UCP – Universal Commerce Protocol

UCP is an open standard co-developed by Google and Shopify [5].

A useful way to think about the difference is that ACP focuses on helping agents complete purchases, while UCP aims to model the entire shopping experience.

It defines standard objects for catalogues, offers, carts, orders, and post-purchase interactions, while supporting things like discounts, loyalty programmes, and fulfilment options.

When a merchant cannot support the full protocol, UCP can fall back to a traditional checkout flow.

UCP is designed to power agent actions on Google AI Mode and Gemini. Shopify uses it for “Agentic Storefronts”, letting merchants sell through those AI surfaces from the Shopify admin [6].

6.3 AP2 – Agent Payments Protocol

AP2 is a Google-led specification that sits underneath UCP as the payments and authorisation layer [7].

Its job is to answer a simple question: how does an agent get permission to spend money?

It defines how agents negotiate payment handlers, mandates, and authorisation flows so they can work across different payment providers and instruments in a consistent way. Without something like AP2, every wallet and PSP would need its own way for agents to request and confirm payments.

6.4 TAP – Trusted Agent Protocol (Visa)

TAP is a Visa initiative developed with partners such as Cloudflare, Microsoft, and several fraud and risk platforms [8]. Its goal is to help merchants distinguish trusted agents from unknown bots.

It gives each vetted agent a cryptographic identity and key pair. Agents sign their requests; Visa and participating merchants verify these signatures against a registry of trusted agents. That lets systems distinguish “known good” agents from generic bots at the network edge.

TAP does not replace ACP or UCP. It operates underneath them as a trust and identity layer for AI-initiated card transactions. Below the commerce layer, network-led schemes such as TAP and Mastercard Agent Pay define how agents are registered, attested, and tokenised on card rails. They live primarily in the trust and payments layer, but they are tightly coupled to how ACP, UCP, and AP2 flows are executed in practice.

By this point, the number of protocols can feel confusing.

A useful way to think about them is that most operate at different layers of the stack.

6.5 So, is there really a “protocol war”?

The phrase “protocol war” suggests these systems are directly competing. In reality, most of them operate at different layers of the stack. ACP and UCP focus on commerce interactions. AP2 and TAP focus on payments, trust, and authorisation. The real question is not which protocol wins, but which combinations become the default choices for merchants, payment providers, and AI platforms.

7. Layers 3–4 – Payments, identity, and instruments

Once an agent has built a cart, something still has to move money.

That raises a question traditional ecommerce never had to answer:

“How does a merchant know an agent is allowed to spend on behalf of a real person or business?”

When you buy something yourself, the answer is straightforward. You log in, complete authentication, and authorise the payment.

Agents complicate that model.

An agent might be buying coffee for an office, booking travel for an employee, or paying for software on behalf of a business. The merchant needs to know who the agent represents, what it is allowed to do, and whether the payment should be approved.

This is the problem payment networks, banks, and infrastructure providers are now trying to solve.

7.1 Payments and identity

Visa and Mastercard are approaching this challenge in similar ways.

Both are building systems that let merchants recognise trusted agents and understand what they are authorised to do.

Visa’s Trusted Agent Protocol (TAP) gives approved agents a cryptographic identity that merchants can verify [8]. Mastercard’s Agent Pay programme takes a similar approach with Agentic Tokens, which carry information about which agent is acting, who authorised it, and what kind of transaction it is allowed to perform [9].

Both networks emphasise that not every agent should be allowed to transact. Agents must first be registered and approved before they can act on behalf of users or businesses.

This has led to the emergence of a new concept: Know Your Agent (KYA). Much like Know Your Customer (KYC), the goal is to establish the identity of the software before it is trusted with financial actions.

Card networks are not the only players entering this space.

Open banking providers are also positioning themselves as infrastructure for agentic commerce. Plaid highlights three areas where AI systems need support: access to financial data, identity verification, and moving money through pay-by-bank or wallet funding flows. TrueLayer takes a similar approach, offering account-to-account payments, variable recurring payments, and even an MCP server that lets AI assistants interact directly with its payment infrastructure.

Rather than converging on a single solution, the industry appears to be moving towards a multi-rail model. Card networks, open banking providers, and newer crypto-native systems are all adapting to a world where software can initiate transactions on behalf of people and businesses.

7.2 Card issuance and wallets

Even in an agentic world, agents still need payment instruments.

One common approach is to give agents their own virtual cards or wallets with tightly controlled spending limits.

Programmable card-issuing platforms already let companies create cards for specific teams, vendors, or workflows. The same idea extends naturally to agents: each agent can receive its own spending rules, merchant restrictions, budgets, and reporting controls.

Corporate spend-management tools already use these mechanisms to automate recurring purchases and policy-driven payments. Agentic commerce simply pushes the model further, giving software more flexibility while keeping the same underlying controls.

In many ways, this layer is the body that lets agents interact with existing payment rails.

8. Layer 5 – Checkout execution: the thin waist

By this point, the agent understands what to buy, has permission to spend money, and has a payment instrument it can use.

The problem is that somebody still has to complete the purchase.

This turns out to be harder than it sounds.

Most ecommerce websites were built for humans, not agents. Checkout flows contain custom forms, hidden business logic, anti-bot protections, and countless edge cases that only make sense when a person is sitting in front of a browser.

Protocols such as ACP and UCP help, but they only work when merchants support them. Much of the web still does not.

This has created a new category of infrastructure focused on what is often called checkout execution.

These companies take a product URL or purchase intent and do whatever is necessary to complete the transaction. Sometimes that means calling APIs. Sometimes it means driving a browser. Often it means handling dozens of edge cases that sit somewhere in between.

Examples include browser-automation and navigation tools such as Bright Data, Browserbase, Browser Use, Exa, Parallel, and Skyvern, alongside API-focused checkout providers such as Firmly, Henry Labs, Rokt, and Rye.

Vertical commerce agents are also becoming important players in this layer. Companies such as Decagon are increasingly moving beyond recommendations and customer support towards workflows that can drive real transactions.

This is one of the hardest layers in the stack.

The vision of “agents can buy anything on the internet” ultimately depends on it. No matter how good the models become, someone still has to bridge the gap between agent intent and the messy reality of existing checkout systems.

9. Layer 6 – Merchant enablement and discovery

Agents cannot buy what they cannot see.

So far we have looked at how agents express intent, communicate with merchants, obtain permission to spend money, and complete purchases.

But before any of that can happen, agents need to discover products and understand what is being sold.

For years, merchants optimised their product data for search engines, marketplaces, and advertising platforms. Increasingly, they also need to optimise it for AI systems.

9.1 Product data as a first-class asset

In an agentic world, product data becomes infrastructure.

Agents need structured information about products, prices, availability, shipping options, and merchant policies. The better that data is organised, the easier it is for agents to understand and recommend products.

This has created two broad categories of tools.

The first focuses on making merchant data easier for agents to consume. Companies such as Catalog, Commerce Clarity, Merchkit, Swap, and Colossal help merchants structure, normalise, and expose product information through APIs.

The second focuses on visibility. GEO and AgentEO platforms such as Bluefish, Chainshift, Peec, Profound, and Wilgot help merchants understand how they appear inside AI-generated answers and improve how agents interpret their products.

The underlying question is simple:

“How do agents see us?”

For many merchants, that question is starting to become as important as:

“How do search engines see us?”

9.2 The coverage gap

There is one problem with this vision.

It assumes merchants participate.

Many do not.

Protocols, feeds, and merchant platforms only cover the businesses that choose to implement them. Large parts of the internet still run on older ecommerce systems, custom software, or regional platforms that were never designed for agents.

As a result, many merchants remain effectively invisible to agents that rely solely on official feeds and protocols.

Bridging that gap is one of the reasons browser automation, middleware, and checkout execution tools have become so important. They allow agents to operate in parts of the web that have not yet become agent-ready.

The result is a fragmented landscape. Some merchants are exposing rich, structured data directly to agents. Others can only be reached through automation and workarounds.

Closing that gap may be one of the biggest challenges in making agentic commerce work at internet scale.

For merchants, the practical implication is straightforward: becoming agent-readable may become as important as becoming search-engine-readable. Product data, inventory, pricing, availability, and policies increasingly need to be exposed in formats agents can understand and act on.

10. Layer 7 – Trust, fraud, and security

By this point, agents can discover products, complete purchases, and move money.

That creates a new problem.

How does anyone know an agent is trustworthy?

For years, most fraud systems operated on a simple assumption: non-human traffic was usually bad traffic.

Agentic commerce breaks that assumption.

Some agents are authorised to act on behalf of real people and businesses. Others are malicious. The challenge is telling the difference.

At a high level, trust in agentic commerce comes down to four questions.

Identity: Which agent is making this request, and who does it represent?

Mandates: What is the agent actually allowed to do?

Integrity: Has the request been altered or tampered with?

Accountability: Can the actions be audited later if something goes wrong?

This represents a shift in how fraud systems work.

Instead of asking:

“Is this a browser?”

systems increasingly ask:

“Is this a permitted agent acting under a valid mandate?”

Protocol-level information such as signatures, mandates, and agent identities is becoming a new source of risk and trust signals.

This has also led to the emergence of a new concept: Know Your Agent (KYA).

Much like Know Your Customer (KYC), KYA aims to establish the identity of software before it is trusted with financial actions. Companies such as Plaid are already positioning KYA as an extension of existing identity and verification infrastructure, while identity and authentication providers are beginning to build agent-specific tools around delegated authority, authentication, and fraud prevention.

The goal is straightforward: give agents a way to prove who they are and what they are allowed to do before merchants, banks, and payment providers let them act.

11. New monetisation models and rails for agents

Most of today’s software pricing and payment rails were built for predictable, human-driven workflows. Agents work differently.

So far, this article has focused on how agentic commerce works.

The next question is what changes economically once software can act on our behalf.

Many of today’s pricing models, payment systems, and business models were designed for humans.

Agents behave differently.

They can work continuously, make thousands of decisions, call dozens of services, and interact with other agents without human involvement. As a result, some of the assumptions that underpin today’s software and payment infrastructure start to break down.

11.1 Why flat SaaS pricing struggles

Traditional SaaS assumes roughly fixed usage per seat.

Agents behave more like workers than users. They may retry, branch, and consume different amounts of compute, APIs, and third-party services while attempting the same task.

That creates two problems.

First, costs become unpredictable. The same task may require very different amounts of work depending on the path the agent takes.

Second, value becomes harder to measure. Many small actions contribute to a final outcome.

As a result, flat per-seat pricing starts to look like a poor fit. Many observers expect a shift towards usage-based or outcome-based pricing, where businesses pay for calls, workflows, or results rather than licences.

A growing group of companies is building the metering and billing infrastructure needed to support this model, particularly for machine-to-machine interactions and AI-native services.

11.2 Why some flows may need new rails

The same challenge appears in payments.

Multi-agent systems often rely on specialised agents to perform narrow tasks: fetching data, scoring risk, resizing images, generating content, and more.

Many of these interactions are frequent and tiny in value.

At that scale, traditional payment rails become awkward. Fixed fees, minimum transaction sizes, chargeback processes, and settlement delays were not designed for thousands of low-value machine-to-machine transactions.

This is one reason interest in new payment rails has grown.

Crypto and stablecoin-based systems are one approach. Standards such as x402 aim to let agents hold balances and settle very small transactions cheaply and programmatically.

Card networks are adapting as well. New token formats, delegated credentials, and mandate systems such as TAP and AP2 are designed to make agent-initiated transactions possible within existing payment infrastructure.

11.3 Open banking as another rail in the mix

Not every agent payment is a micro-payment.

Many agentic transactions look much closer to traditional ecommerce purchases, subscriptions, and B2B payments than to machine-to-machine settlement.

This is where open banking becomes interesting.

Open banking providers such as Plaid and TrueLayer already enable account-to-account (A2A) payments and wallet funding with lower and more predictable merchant fees than many card setups, alongside strong customer authentication by design. TrueLayer cites typical merchant fees below 1% for open banking payments, with no separate card-terminal, PCI, or chargeback fees [10]. Plaid positions its infrastructure for AI companies around three jobs: permissioned access to data, identity and KYA, and pay-by-bank or wallet funding for agentic journeys [11].

For a single consumer purchase or B2B payment initiated by an agent, A2A rails can be a practical alternative to cards.

Taken together, open banking and card networks represent one path for agentic payments: adapting existing financial infrastructure so agents can transact safely on behalf of users and businesses.

11.4 No single winner yet

In 2026 there is no clear winner among these rails.

Card networks remain deeply embedded in global commerce and are adapting through initiatives such as TAP and Agent Pay. Open banking providers are growing quickly in ecommerce and subscription payments and are natural candidates for many agent-initiated account-to-account flows. Crypto-native systems and new protocols are targeting categories of transactions that traditional payment rails were never designed for, particularly high-frequency machine-to-machine interactions.

The more interesting question may not be which rail wins, but which rail becomes the default way agents move money.

A realistic view is that agents will need to speak multiple rails. Successful infrastructure will make it easy to combine them, choose the right rail for each use case, and route transactions intelligently across them.

12. Where value may accrue

Much of the discussion around agentic commerce focuses on the agents themselves.

But the history of technology suggests that value does not always accrue where attention is highest.

The most interesting question may not be who builds the best shopping agent, but who owns the infrastructure underneath.

One reason is that agentic commerce changes how payments are initiated.

Traditional payment systems were designed around human decisions. A person decides to buy something, authorises a transaction, and completes a checkout.

Agents introduce different behaviour. They can monitor prices continuously, make purchases automatically, coordinate with other agents, and potentially execute large numbers of low-value transactions.

That creates pressure for new forms of identity, authorisation, trust, and payment infrastructure.

Different parts of the industry are already responding. Card networks are extending existing infrastructure for an agentic world. Open banking providers see an opportunity to become a new rail for agent-initiated payments. Crypto-native systems are targeting categories of transactions that traditional payment networks were never designed to handle.

This possibility is no longer just attracting startups. The UK’s Financial Conduct Authority has already identified agentic commerce as an emerging shift in how decisions and transactions are made, while major payment networks have spent the last few years investing heavily in open banking infrastructure and alternative payment rails [12].

The opportunity may not be replacing existing networks. It may be becoming the default layer through which agents move money, prove identity, obtain permission, and interact with merchants.

In an agentic world, moving money may become only one part of the job. Identity, delegated authority, trust, and routing across multiple rails may become just as important as the payment itself.

In many ways, this is the first serious challenge in years to some of the assumptions that underpin online payments. If software increasingly decides when to buy, how to pay, and which merchant to choose, then control may shift towards the infrastructure layers that agents rely on.

This pattern is already visible in the startup ecosystem. Large numbers of companies are building agents. Far fewer are solving the infrastructure problems underneath them. Checkout execution, trust, KYA, observability, metering, and agent-native payments remain difficult and relatively under-served categories despite being some of the hardest problems in the stack.

In that world, some of the most valuable companies may not be the agents themselves.

They may be the companies building the rails underneath them.

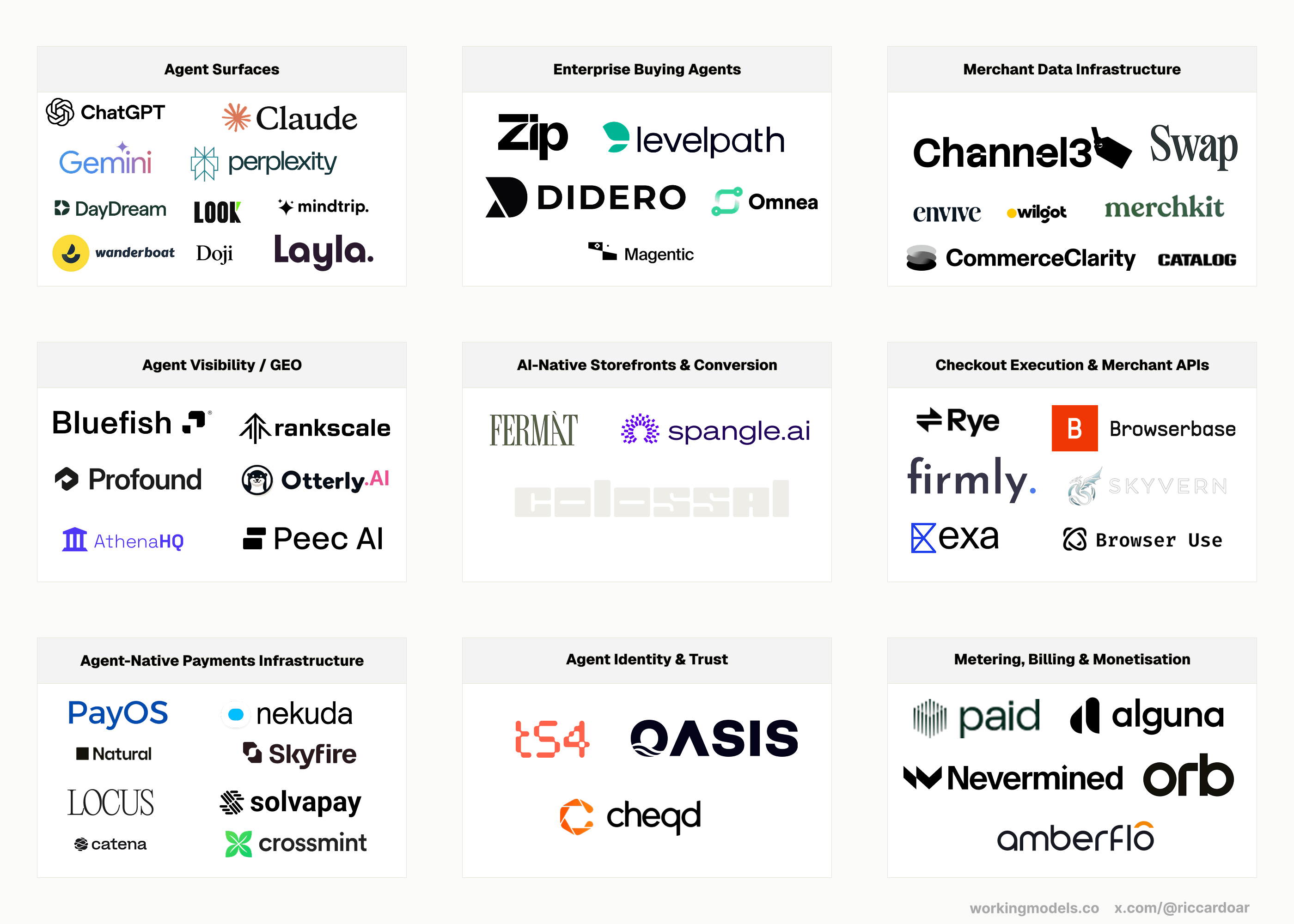

13. Startup landscape: who is building each layer?

By this point, the stack should be familiar.

The final piece is understanding where companies are being built.

The market map below is illustrative rather than exhaustive. The goal is not to list every company. It is to show where activity is concentrated today.

Some categories are already crowded. Agent surfaces, enterprise buying agents, and GEO platforms have attracted significant attention and funding over the past two years.

Others remain surprisingly sparse. Agent identity, trust, metering, and agent-native payments contain relatively few specialised companies despite being some of the hardest problems in the stack.

A note on scope. This map focuses mostly on startups. Large incumbents such as Stripe, Plaid, TrueLayer, Visa, Mastercard, and Coinbase are intentionally excluded even though they play an important role in the ecosystem.

The main exception is AI-native surfaces such as ChatGPT, Claude, Gemini, and Perplexity. They are included because they have become some of the primary places where product discovery and purchasing journeys begin.

The exact company list will change quickly. The more important observation is that agentic commerce is no longer a single market. It is becoming an ecosystem of specialised categories, each solving a different part of how software discovers products, moves money, establishes trust, and completes transactions.

14. Practical implications

For merchants, the immediate priority is becoming agent-readable. Product data, inventory, pricing, and policies increasingly need to be exposed in formats agents can understand and act on. Agents may become a meaningful new source of demand, but they may also shift influence away from traditional marketing and towards algorithmic decision-making.

For payment providers, the challenge is no longer simply moving money. It is enabling software to move money safely. Identity, delegated authority, trust frameworks, and support for multiple payment rails are becoming increasingly important.

For startups, the most obvious opportunities may not be where attention is highest. Large numbers of companies are already building agents. Far fewer are solving the infrastructure problems underneath them. Checkout execution, trust, KYA, observability, metering, and agent-native payments remain difficult and relatively under-served categories.

As with most platform shifts, the biggest opportunities may come from solving one painful problem extremely well rather than trying to own the entire stack.

15. What is real in 2026, and what is still missing

The easiest mistake to make when reading about agentic commerce is to assume it is still mostly a vision.

It isn’t.

Major AI platforms can already drive product discovery and, in some cases, complete purchases through ACP and UCP-based flows. Payment networks have launched trust frameworks such as TAP and Agent Pay. Merchant platforms, product-information tools, and open banking providers are actively adapting their infrastructure for agents.

Perplexity’s “Buy with Pro” feature is a useful example of what this looks like in practice. Users can discover products, compare options, and complete purchases from inside the assistant itself. It is not yet the dominant way people shop, but it demonstrates that the core pieces of the stack can already work together [16].

Google’s agentic checkout takes a different approach. Users can specify a target price and let an agent complete a purchase automatically once the condition is met. Like Perplexity, it demonstrates that agent-driven purchasing is moving beyond prototypes and into real consumer products [17].

What is missing is not capability. It is coverage.

Most merchants still do not support agent-native protocols. Trust frameworks only cover agents that have been explicitly onboarded. Product data quality remains inconsistent. KYA, observability, metering, and checkout infrastructure are still immature in many parts of the market.

The result is a familiar pattern.

The technology is ahead of the infrastructure.

Much of the work over the next few years will be less about making models smarter and more about making the ecosystem around them reliable.

16. Closing

The simplest way to think about agentic commerce is that software is moving from recommending purchases to making them.

That shift sounds small, but it touches almost every layer of commerce.

Agents need ways to discover products. Merchants need ways to expose information. Payment systems need ways to delegate authority. Trust systems need ways to distinguish legitimate agents from malicious ones. Entirely new questions emerge around pricing, billing, identity, and payment rails.

Most of the individual pieces now exist.

What does not exist yet is a fully connected system.

The protocols are still evolving. Trust frameworks are still being adopted. Payment providers are experimenting with new rails. Merchants are still learning how to expose products to agents. Startups are racing to fill the gaps between layers.

The easiest mistake is to assume that the remaining challenges are primarily about AI.

My view is that the hardest problems are increasingly infrastructure problems.

The industry has spent the last few years asking whether software can understand what we want. Increasingly, the answer appears to be yes.

The harder question is whether we can build the systems that allow software to act safely, reliably, and economically on our behalf.

That question may determine where value accrues in the next phase of the market.

Much of the attention today is focused on the agents themselves. But history suggests that attention and value do not always end up in the same place.

If agentic commerce grows as many expect, some of the most important companies may not be the ones building the smartest agents. They may be the ones building the infrastructure underneath: identity, trust, payments, checkout execution, product data, and observability.

Agentic commerce in 2026 still feels early. Adoption remains limited. Large parts of the stack are unfinished.

But for the first time, the shape of the system is visible.

And once you can see the shape, it becomes much easier to see where the next decade of work will happen.

This is a working view, not a definitive one.

If you’re building something in agentic commerce, researching the space, or think I’ve missed an important company or category, I’d love to hear from you.

You can reach me on X, LinkedIn, or by email.

References

[1] Google Developers, “Google Universal Commerce Protocol (UCP) Guide”, 2026. https://developers.google.com/merchant/ucp

[2] CB Insights, “The Agentic Commerce Market Map”, 2025. https://www.cbinsights.com/research/report/agentic-commerce-market-map/

[3] AgenticCommerce.dev, “Agentic Commerce Protocol”, 2025. https://www.agenticcommerce.dev

[4] Stripe, “Introducing our agentic commerce solutions”, 2025. https://stripe.com/blog/introducing-our-agentic-commerce-solutions

[5] Shopify, “Commerce for Agents – Universal Commerce Protocol”, 2026. https://www.shopify.com/ucp

[6] Shopify, “Universal Commerce Protocol – Developer Guide”, 2026. https://www.shopify.com/uk/ucp

[7] Google, “Agent Payments Protocol (AP2) overview”, 2025. https://ap2-protocol.org/

[8] Visa, “Visa Trusted Agent Protocol: Securing AI Commerce Transactions”, 2025. https://digital.nemko.com/news/visa-trusted-agent-protocol-ai-commerce

[9] Mastercard, “Mastercard Agent Pay: secure, scalable and trusted payments in agentic commerce”, 2026. https://www.mastercard.com/us/en/business/artificial-intelligence/mastercard-agent-pay.html

[10] TrueLayer, “4 reasons open banking payments are ready to challenge card payments”, 2021. https://truelayer.com/blog/ecommerce/is-open-banking-the-future-of-ecommerce-payments-4-reasons/

[11] Plaid, “AI in financial services: The rise of intelligent finance”, 2026. https://plaid.com/resources/ai/artificial-intelligence-in-financial-services/

[12] FCA, “Supporting fintech in the next phase of innovation”, 2026. https://www.fca.org.uk/news/speeches/supporting-fintech-next-phase-innovation

[13] Visa, “Visa to Acquire European Open Banking Platform Tink”, 2021. https://investor.visa.com/news/news-details/2021/Visa-To-Acquire-European-Open-Banking-Platform-Tink/default.aspx

[14] Mastercard, “Mastercard to Acquire Finicity to Advance Open Banking Strategy”, 2020. https://www.mastercard.com/global/en/newsroom/press-releases/2020/june/mastercard-to-acquire-finicity-to-advance-open-banking-strategy/

[15] Mastercard, “Mastercard expands open banking reach with acquisition of Aiia”, 2021. https://www.mastercard.com/global/en/newsroom/press-releases/2021/september/mastercard-expands-open-banking-reach-with-acquisition-of-aiia.html

[16] Perplexity, “Buy with Pro: shopping inside Perplexity”, 2024–2025 coverage of launch with Shopify and Stripe (late 2024), expansion to PayPal and Venmo (2025), and integration with Firmly.

[17] Google Blog, “Let AI do the hard parts of your holiday shopping”, 13 November 2025. https://blog.google/products-and-platforms/products/shopping/agentic-checkout-holiday-ai-shopping/